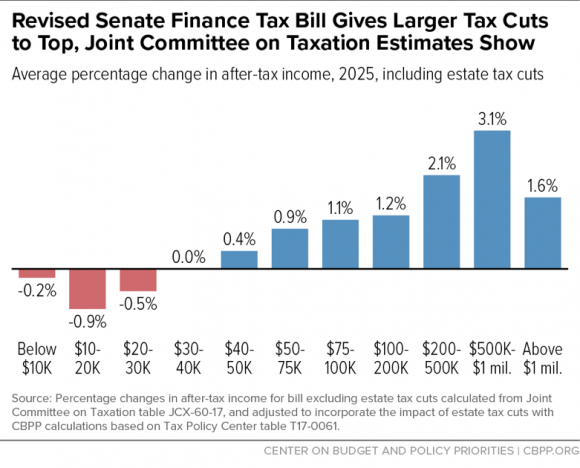

As noted in this earlier post, the distributional consequences of the House Tax Cuts and Jobs Act should include the spending cuts. According to CBO, there will be a $25 billion cut to Medicare unless independent legislation is passed. From TPM:

…automatic cuts spring into action anytime Congress passes a bill that balloons the federal deficit, as the tax bill would. The approximately $136 billion in cuts spurred by the GOP tax bill would hit a number of government programs—including farm subsidies and the Border Patrol—but would cut most deeply into Medicare. Medicaid, Social Security, and food stamps are protected.

Continue reading →