The external sector weighs in, and thinking about the length of the recovery.

More on U.S. Employment, Post-Trough

Reader rtd states “it is virtually guaranteed that after a nation’s business cycle trough, that same nation’s employment growth will display an upward trend.” I thought this an interesting enough assertion that it merited additional investigation.

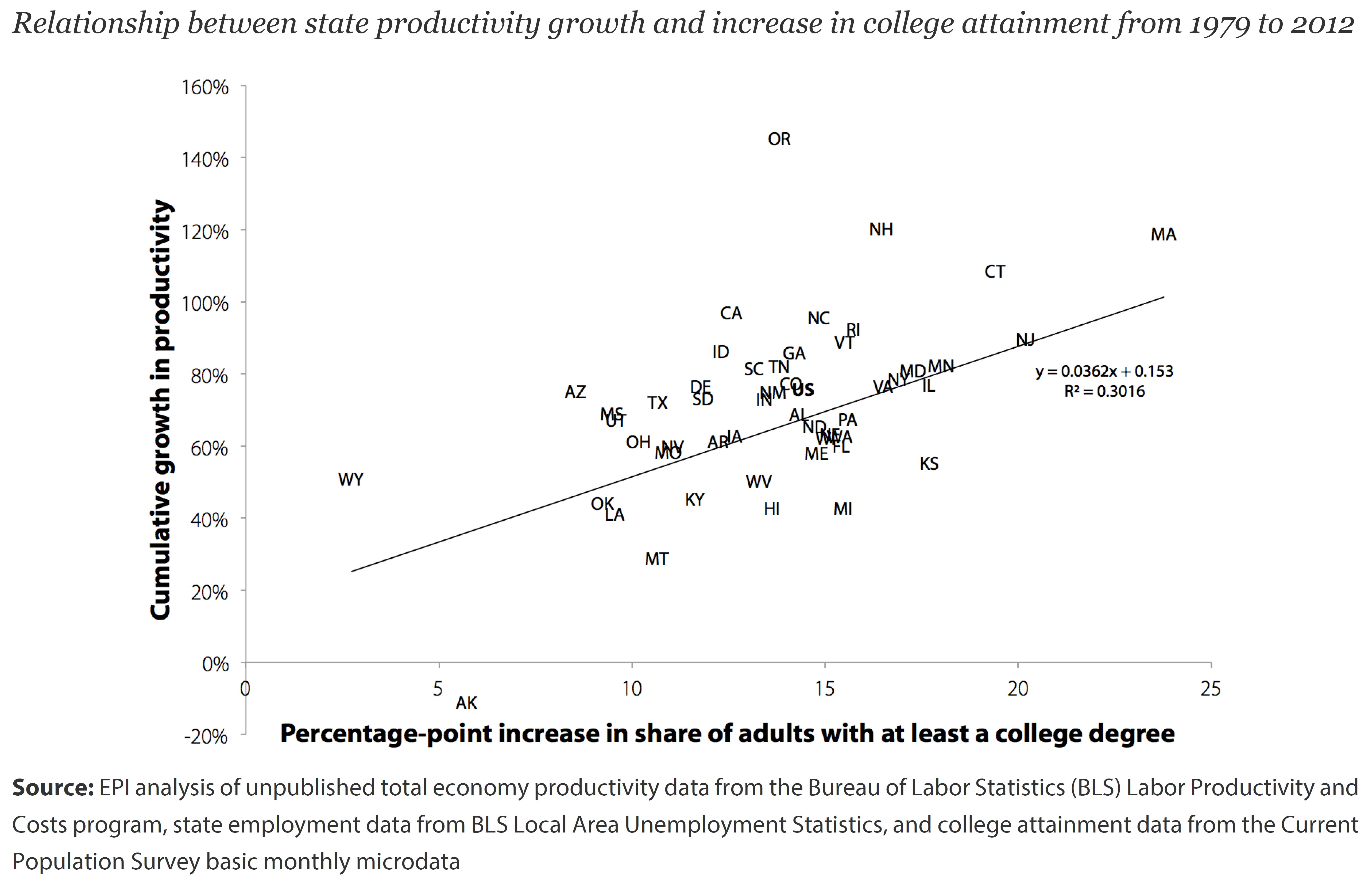

Implications for Economic Growth of Governor Walker’s Proposed Higher-Ed Funding Cuts

From Foxnews:

Wisconsin Gov. Scott Walker is calling for steep cuts to the University of Wisconsin System, while offering the network more freedom in exchange, … [H]is university plan … would cut funding by $300 million over two years…

Source: Berger-Fisher (2013).

The Economics of China, and More

Two extremely useful books on China and the Chinese Currency: The Oxford Companion to the Economics of China and Renminbi Internationalization: Achievements, Prospects, and Challenges.

What’s driving the price of oil down?

In December I provided some simple calculations of the extent to which a slowdown in the growth of global oil demand may have contributed to the spectacular drop in oil prices since last summer, and I updated those estimates two weeks ago. Some of you have suggested that as conditions keep changing, perhaps I should update those calculations every week. Thanks to the always-helpful Ironman at Political Calculations, I can now go that a step better, and provide eager Econbrowser readers a quick tool they can use to update these calculations on their own on a daily basis, if your heart so desires.

Quasi-Stylized Facts about Employment after Troughs

Reader rtd writes: “…it is virtually guaranteed that after a nation’s business cycle trough, that same nation’s employment growth will display an upward trend”, but when asked about the euro area, argues “The Eurozone is a conglomerate of nations with varying fiscal policies, ideologies, cultures, and the list goes on and on. Please don’t compare apples with hand grenades.”

Private Employment under Obama and Bush

Reader Move On admonishes me to … move on. So here is job creation in this Administration, in comparative perspective.

Wisconsin: Only 93,200 Net New Jobs Needed in January 2015 to Hit Governor Walker’s 250,000 Jobs Target

According to WI DWD statistics released today.

Guest Contribution: “Measuring the On-going Changes in China’s Capital Controls”

Today we are fortunate to have a guest contribution by Jinzhao Chen (Paris School of Economics) and XingWang Qian (SUNY Buffalo State). This post is based on this paper.

Guest Contribution: “What Drives Housing Dynamics in China?”

Today we are fortunate to have a guest contribution written by Timothy Bian (University of International Business and Economics, China) and Pedro Gete (Georgetown University).

Continue reading