Today, BLS released data for July. Nonfarm payroll employment growth of 165,000 exceeded expectations of 100,000 (Bloomberg). However, overall, employment indicators continue to rise only slowly.

Kevin “Dow 36,000” Hassett et al. Critique the Tax Policy Center Study

From Boston.com:

On a conference call with reporters, Romney advisers ripped the study — conducted by the Tax Policy Center, a joint venture of the Brookings Institution and the Urban Institute — as “biased” and “a joke.”

The Fed stands pat, at least for now

Today’s statement from the FOMC, the decision-making body for the Federal Reserve, basically said that, yes, the economy has worsened since the FOMC’s previous meeting, but no, they’re not going to do anything about it. At least, not right now.

“Slow Recovery or Failed Agenda?”

That’s the question posed in the title of yesterday’s op-ed by Ed Lazear, and it’s an excellent question. Looking at the statistics, 13 quarters after the President’s inauguration, non-defense GDP is only 4% higher (in log terms) than when he came into office.

Yet another discouraging GDP release

The Bureau of Economic Analysis reported Friday that U.S. real GDP grew at an anemic 1.5% annual rate during the second quarter. When the same bad thing keeps happening to you again and again, “disappointed” no longer seems the appropriate word to use.

We Can Emulate the UK (GDP-wise)!

Or, still no expansionary fiscal contraction in the UK (surprise!)

The UK experiment [0] continues, apparently not too successfully, according to statistics from the UK Office of National Statistics. One picture suffices.

Guest Contribution: Rejoinder to “Oil Price Spike Exacerbated by Wall Street Speculation?”

Today, we are fortunate to have Luciana Juvenal and Ivan Petrella, as guest contributors. In this post, they respond to Wednesday’s guest contribution by Lutz Kilian, entitled Oil Price Spike Exacerbated by Wall Street Speculation?.

Guest Contribution: “Oil Price Spike Exacerbated by Wall Street Speculation?”

A recent study by Luciana Juvenal and Ivan Petrella suggests that the financialization of oil futures markets contributed significantly to the surge in oil prices after 2003. Lutz Kilian, Professor of Economics at the University of Michigan, questions their analysis and highlights that their paper actually does not shed any light on the role of Wall Street speculation.

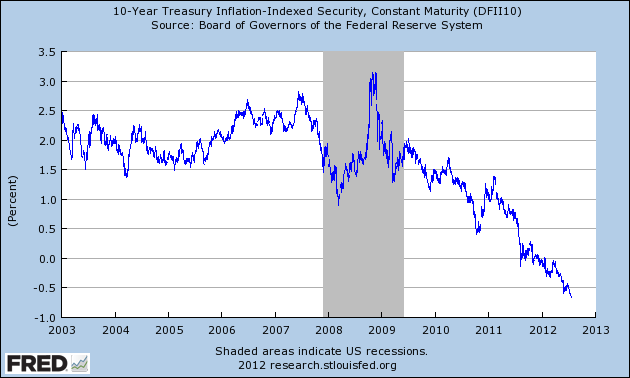

Crowding Out Watch: July 2012

As feared by Representative Ryan, in March 2011, crowding out due to deficits: The ten year inflation adjusted constant maturity rate as of 7/20 was -0.67%

Source: St. Louis Fed FRED accessed 7/24 11am Pacific.

The Path Not Taken … Thus Far: Debt Deleveraging by Inflation

From the latest issue of the Milken Institute Review, “Trends: Better Living Through Inflation” (co-authored with Jeffry Frieden):