For EPU through yesterday, news sentiment through 5/18.

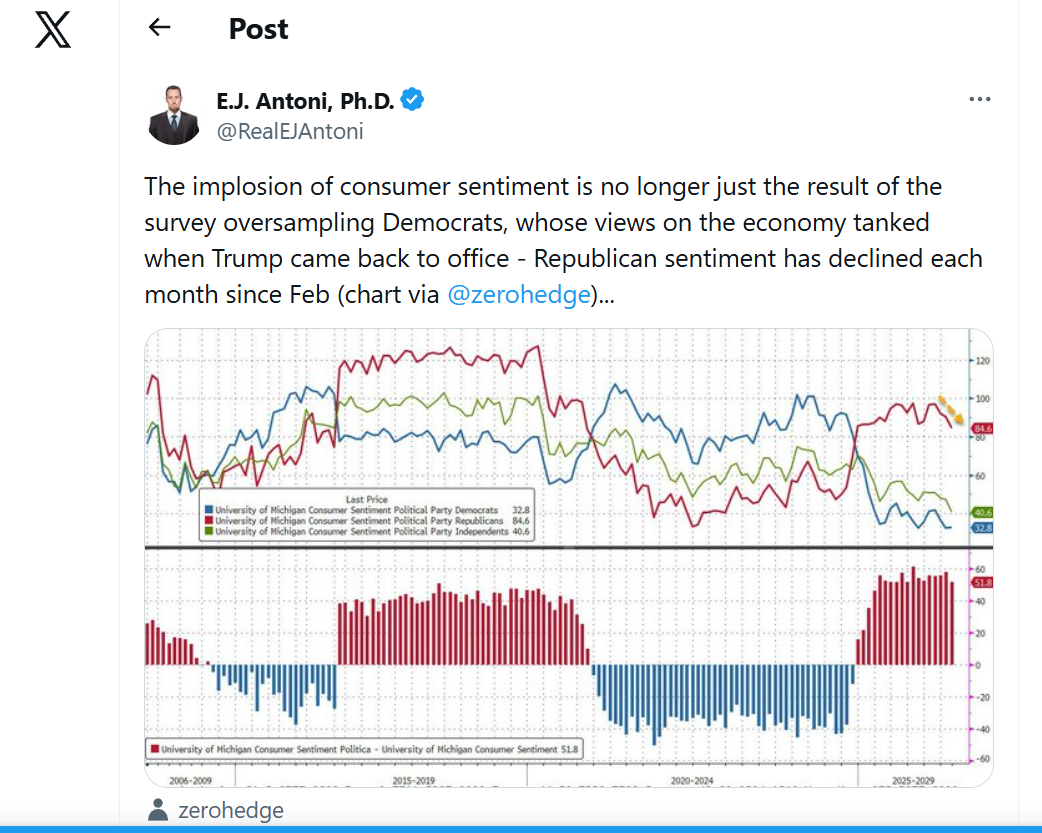

Did U.Mich Sample Overweighting of Democrats Lead to a Biased Reading on Sentiment, Pre-March?

That’s an assertion by EJ Antoni.

Well, in Director Judy Hsu’s May report, she tackles this issue directly.

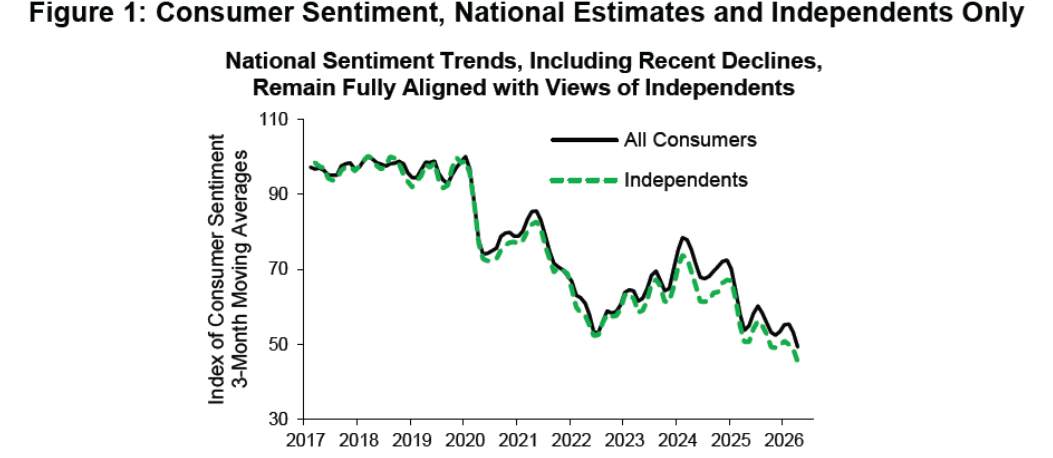

The April 2025 report, “Partisan Perceptions and Sentiment Measurement,” discusses how partisan differences do not distort the national survey estimates of changes over time. A year later, amid historically rapid changes in the public policy landscape, partisan gaps in sentiment are now even larger while national sentiment has trended down in recent months. Are the relatively dour readings seen in recent months being disproportionately driven by Democrats? A closer inspection of data on multiple dimensions of the economy reveals a resounding no.

Sentiment readings nationally (both on a level and trend basis) continue to be fully aligned with the views of independents, as seen in Figure 1. Looking specifically at 2025 and 2026, the time path of sentiment continued to be virtually identical for independents compared with all consumers nationwide: the broad plummeting of national sentiment between January and April/May as tariff announcements escalated; its improvement thereafter as tariff rhetoric calmed down; and the downtick seen in the wake of the Iran conflict. For independents as well as all consumers, May 2026 readings are lower than their respective June 2022 troughs.

….

This report was posted at the same time as the final data was published, so Dr. Antoni has no reason to have missed it, unless he was in a hurry, sloppy, or both.

I investigated whether Sentiment determinants differed substantially between overall (FRED mnemonic UMCSENT) and Sentiment for Independents, using the unemployment rate, y/y inflation rate, and SF Fed news sentiment (u, π, and newssent respectively).

sent = 82.59 – 0.03u – 2.70π + 31.31newssent + 8.17trump

Adj-R2 = 0.37, SER 13.18, DW = 0.114, NObs = 111, 2017M02-2026M05, bold denotes significant at 10% using robust standard errors.

sentInd = 77.35 – 0.05u – 2.24π + 30.92newssent + 10.96trump

Adj-R2 = 0.36, SER 14.49, DW = 0.125, NObs = 111, 2017M02-2026M05, bold denotes significant at 10% using robust standard errors.

There is no discernable difference in the results.

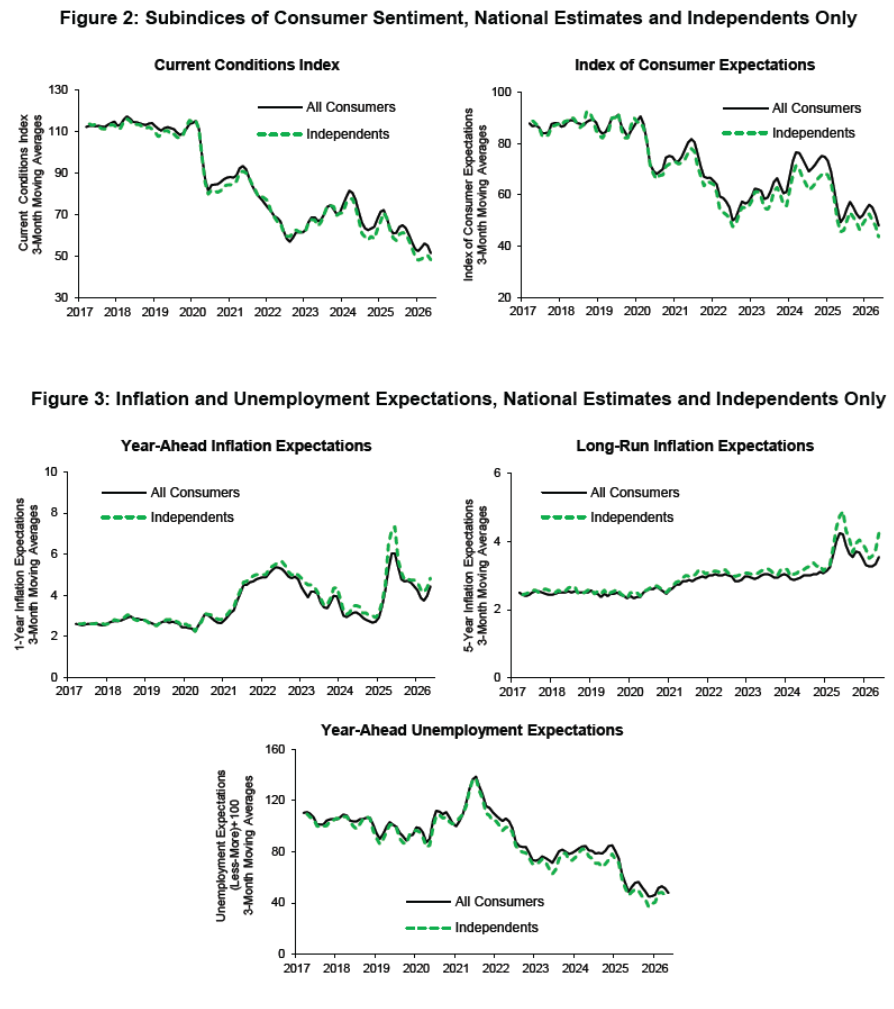

The alignment across all sorts of other dimensions is clear in the graphs:

If anything, the “all consumers” readings before March 2026 were more optimistic than independents readings, save year-ahead unemployment expectations.

I’m not arguing that there’re no problems with the U.Mich series; Cummings and Tedeschi (2024) find a structural break associated with the switch to online sampling (see here). I find that only about half of the deviation from observables is attributable the switch. But this doesn’t appear prima facie to be a problem of oversampling Democrats/Lean Democratic.

Detrended Sentiment

Using the HP filter applied to U.Michigan Sentiment, consumers don’t seem too gloomy relative to “average”. But they do seem gloomy relative to observed unemployment and inflation rates.

Inflation Expectations Short and Long: Up

From today’s U.Mich release, final 1 yr revised up from 4.5% to 4.8%, and 5 yr revised up from 3.4% to 3.9% (!).

U.Mich Sentiment, Gallup Confidence Plunge

May Michigan Sentiment downwardly revised from preliminary, to a record low.

Why the February CBO Baseline Debt Will Be Off

In a previous post, I noted that the February CBO projection of debt would likely be an underestimate, and perhaps increasingly so over time, suggesting upward pressure on rates.

“From Bust to Boom: Stock Market Participation and the Housing Boom”

That’s the title of a paper by Yanshuo Chen, (PhD, UCSC):

Who Holds Federal Debt As of March 30

Let’s hope foreign non-official sector wants to hold on to US government debt.

Where Should the 10 Year Treasury Rate Be?

Debt issuance is rising, foreign official holdings of Treasurys are falling, the Fed is reducing holdings, and expected inflation is rising. How well do we predict rates?

The Change in 10 Year Yields: Up, Up and Away

Treasurys and TIPS, 70 and 46 bps respectively.

Continue reading