The economy plugs along much as it did before the election, while the stock market hits new highs. What about other variables?

“What’s the Problem with Low Inflation?”

That’s the title of a new EconoFact article by Michael Klein.

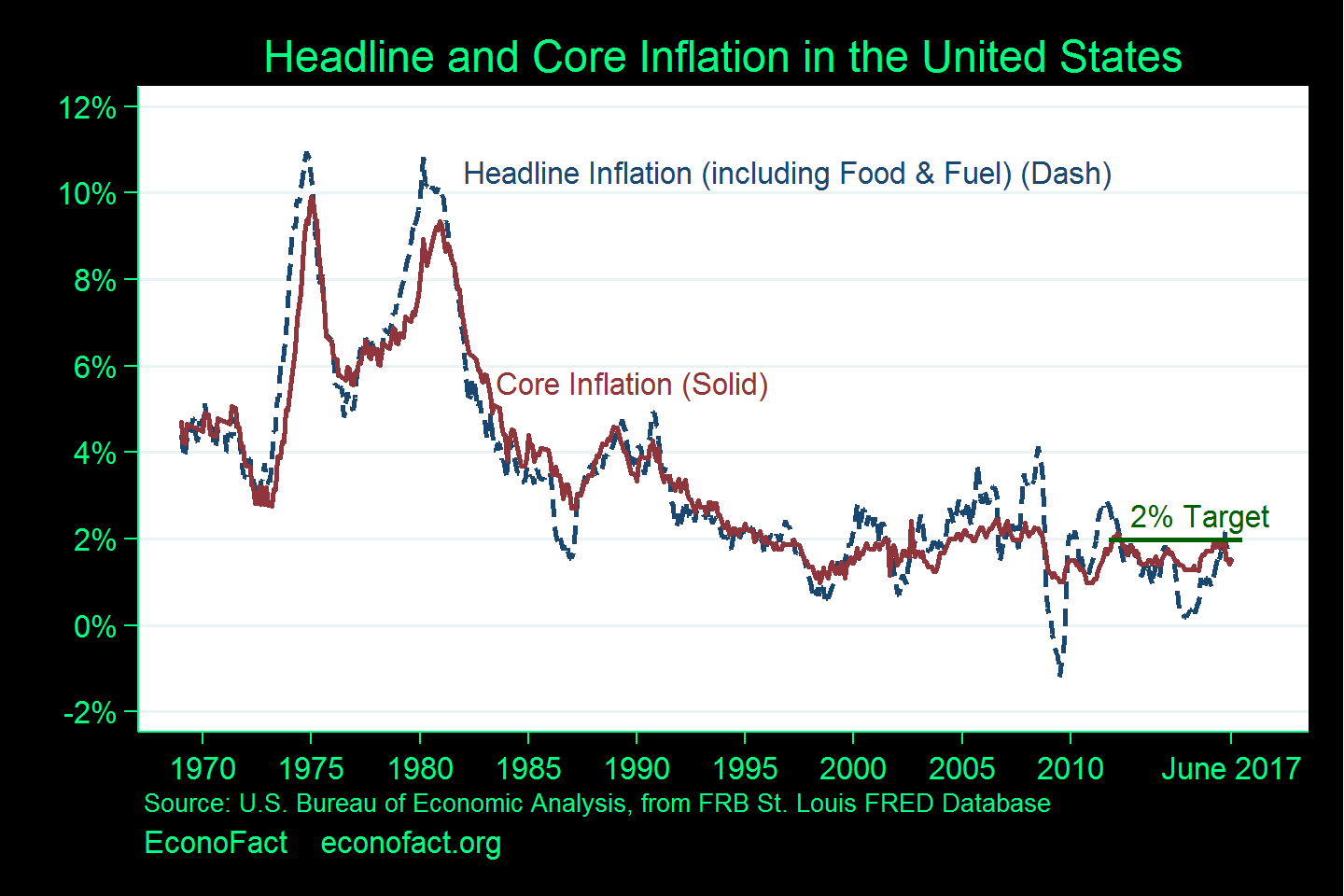

Today’s low inflation has some economists puzzled. The Federal Reserve has persistently undershot its inflation target of 2 percent since 2012, when it established this level of inflation as one of its policy goals.

…

Low inflation can be a signal of economic problems because it may be associated with weakness in the economy. When unemployment is high or consumer confidence low, people and businesses may be less willing to make investments and spend on consumption, and this lower demand keeps them from bidding up prices.…

There have been calls for the Federal Reserve to raise interest rates because the ongoing recovery from the Great Recession represents the third-longest recovery on record and the current low unemployment rate would usually lead the Federal Reserve to set its policy course towards preventing the economy from overheating. It is striking, however, that this recovery has not been accompanied by increasing inflation, even with unemployment rates of 4.3 percent in June and July, the lowest string of two-month unemployment rates in more than 15 years.

This figure from the article highlights the anomalous nature of recent inflation behavior.

Source: Klein.

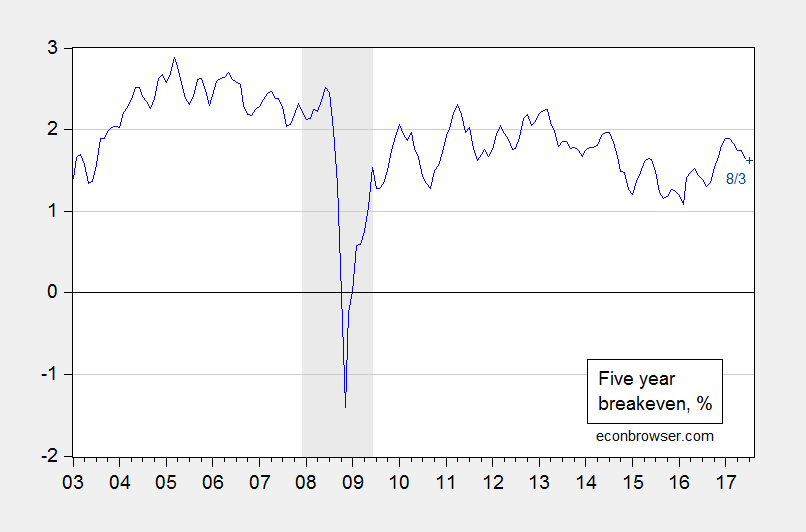

What are the prospects for accelerated inflation? The market’s expectation inferred from Treasury spreads is shown below:

Figure 1: Five year nominal Treasury yield minus five year TIPS yield, % (blue). July 2017 observation (dark blue +). Source: Federal Reserve Board.

As noted, such quiescent current and expected inflation at (what is widely acknowledged to be) near full employment does pose something of a mystery.

In the past, I’ve argued that the inflation target should be higher than the current 2%. [1] [2] I still believe that’s the case.

What’s the Dead Weight Loss of a Consumption Tax When Externalities Are Present?

Guest Contribution: “Central Banks: From Triumph to Crisis and The Road Ahead”

Today we are pleased to present a guest contribution written by Pierre Siklos, Professor of Economics at Wilfrid Laurier University.

U.S. begins ninth year of economic expansion

The Bureau of Economic Analysis announced today that U.S. real GDP grew at a 2.6% annual rate in the second quarter. That is below the long-term historical average of 3.1%, but better than the 2.1% we’ve seen on average since the Great Recession ended in 2009.

Continue reading

Beware the State Level Household Employment Series: Wisconsin Edition

Steve Kopits obsesses on the household survey based employment series for Wisconsin, despite our previous exchange on why reliance on this series for Kansas is a problem. But just to make matters concrete, lets look at a few vintages of the household series.

Guest Contribution: “Why the Republicans Can’t Reform Health Care”

Today, we present a guest post written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. A shorter version appeared in Project Syndicate.

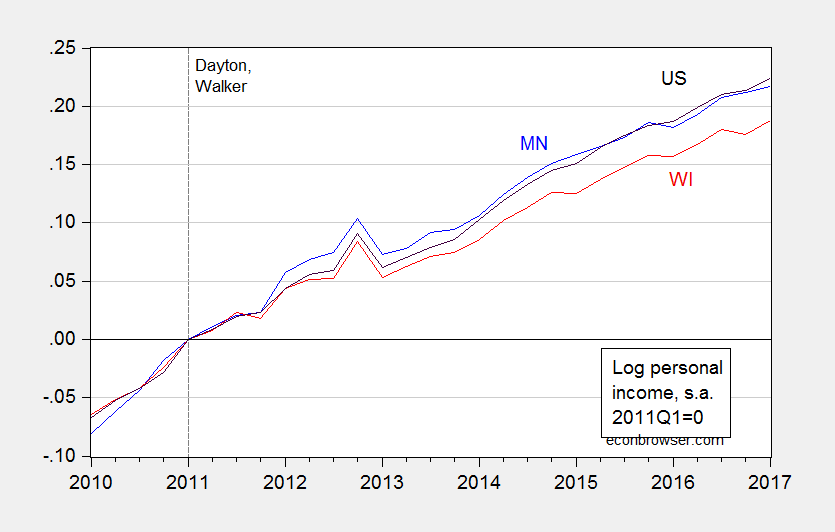

Context Is Important: More on MN vs. WI

Reader Jesse Livermore thinks he’s discovered Wisconsin is in actuality doing really well vis a vis Minnesota. He writes:

Wisconsin personal income growth dramatically outperformed Minnesota in Q1.

Well, I’ll just say the level is sometimes just as important as the first derivative. That’s why I plot time series, rather than just quoting a quarter’s worth of growth. Here is a comparison of personal income over the past few years.

Figure 1: Log nominal personal income for Minnesota (blue), Wisconsin (red), and US (black), all normalized to 2011Q1=0. Source: BEA, June 27, 2017, and author’s calculations.

On a per capita basis, cumulative Minnesota personal income growth remains 0.7 percent higher (log terms) than Wisconsin’s. It has been higher since 2011Q1.

My advice to anyone trying to assess relative economic performance: plot the time series.

Wisconsin Nonfarm Payroll Employment Continues to Decline

And lags further behind its neighbor Minnesota. Wisconsin nonfarm payroll (NFP) employment is now below April 2017 peak. Finally, employment lags what would be predicted from the historical correlation of Wisconsin employment with national.