From NBER today:

The Business Cycle Dating Committee of the National Bureau of Economic Research maintains a chronology of the peaks and troughs of US business cycles. The committee has determined that a trough in monthly economic activity occurred in the US economy in April 2020. The previous peak in economic activity occurred in February 2020. The recession lasted two months, which makes it the shortest US recession on record.

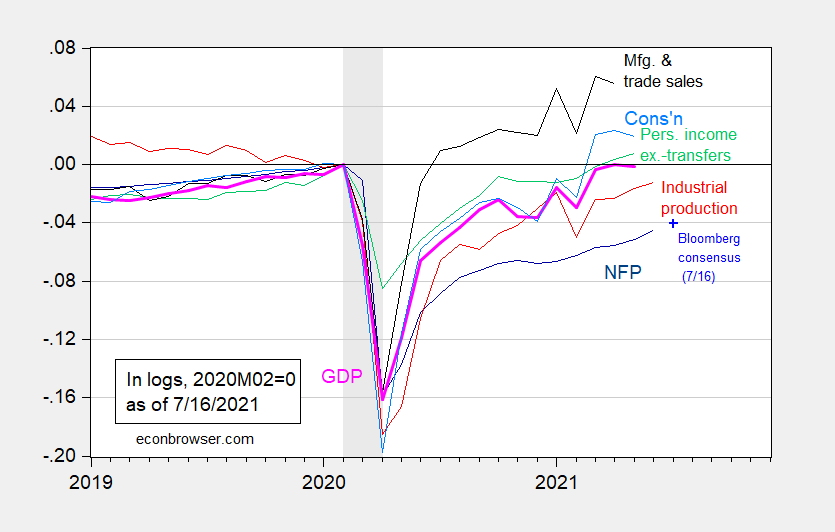

Here is the resulting graph (monthly) showing some key indicators:

Figure 1: Nonfarm payroll employment from June release (dark blue), Bloomberg consensus as of 7/16 for July nonfarm payroll employment (light blue +), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (7/1/2021 release), NBER, and author’s calculations.

ECRI places the business cycle monthly peak at February 2020, and for growth rate cycles, peak at December 2017 and trough at April 2020.

For quarterly data, peak is at 2019Q4, trough at 2020Q2.

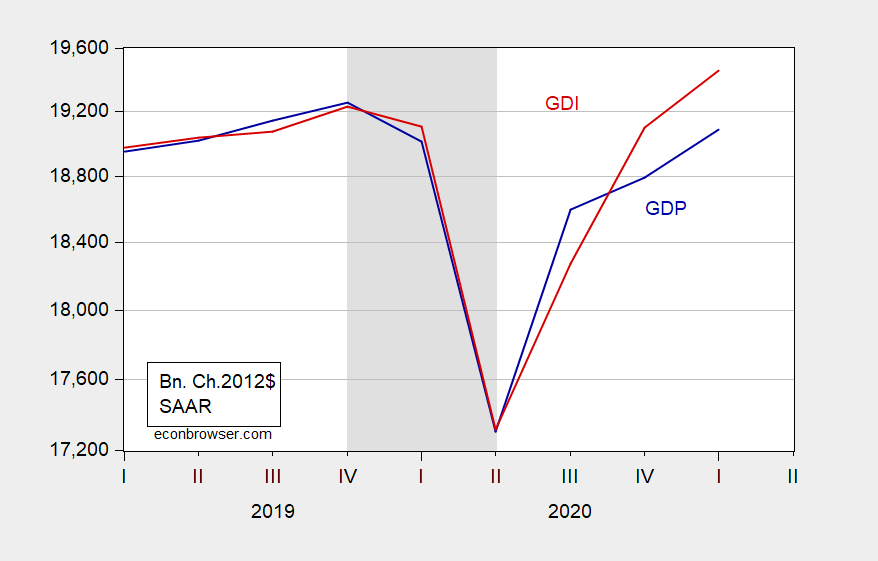

Figure 2: GDP (blue) and GDI (red), both in billion Ch.2012$, SAAR. NBER recession dates shaded gray. Source: BEA, 2021Q1 3rd release, NBER.

Chronologies for other countries, see this post.

Update, 7/20, 11:50am Pacific:

See also https://www.bloomberg.com/news/articles/2021-07-19/u-s-recession-in-2020-lasted-two-months-academic-panel-says

Menzie gave me a heads up (trough/peak length of recession) on this, and of course Menzie ended up being correct, as we see here from NBER today. I felt then, and I still feel now, that it doesn’t make economists look good from a public relations standpoint, and communications standpoint to say “the Covid-19 recession only lasted 2 months”. Now if Academic (and otherwise type of credentialed economists) want the general public to laugh at/ignore/disregard/slough-off what they say then they can go around telling people “this last recession only lasted 2 months”. That’s fine if an economist wants to say that. Just don’t expect people to respect what credentialed/professional economists say from that point on. Because the general public is never going to respect you when you go around writing or saying things like that.

I’m stating facts here, pragmatic realities. If that offends any professional/academic economists out there I suggest you write a longform letter which starts out “Dear Human Nature……… ” and see what reply you get back.

Moses Herzog: Well, should historians tailor their decisions to gain credibility with people. Should a historian say gloss over the imposition of poll taxes in the South in order to get credibility with those who believe those who can’t pay don’t deserve to vote.

In any case, the disjuncture between what constitutes a “recession” amongst the people who developed the expansion/contraction chronology, and ordinary people has long existed. I would say the difference is between recession (gradient) and output gap (level relative to trend).

Your point is valid. I know it’s hard to do these things and “make everyone happy”. I also know a good many economists like to stay away from “value judgements” because it can muddy the waters on objectivity. But when a profession of people, or one of that profession’s more respected institutions tells people “the recession ended at the trough” (April 2020), that just doesn’t cut it for me, and I think it’s even borderline invalid. There has to be a new way to measure if you want people to regard those numbers with any kind of seriousness.

Just a a more extreme example (frankly I think the current 2020–2021 context is more than enough to illustrate how bad this is, saying “it was two months”). I’ll use a more extreme example for arguments sake. You’ve discussed “L” recessions. Now these letter nicknames for recession types, don’t always fit exact right?? But let’s say you had an “L” but let’s say the bottom part of that L only raised slightly, very very slightly. So if you had a 180 degree arc (like a protractor you used in grade school) the far right is 0, the far left is 180 degrees. And the line of the bottom of that “L” recession (“the bottom portion of the L”) was like 10 degrees above a horizontal line or maybe even just 5 degrees off a horizontal line, so the recovery shoots off at a 5 degree angle to the right. You’re going to tell me the “end of the recession” is where the lines break-off and the line shoots off at a 5 degree angle to the right?? After a near straight drop down, or a “steep slope downward” if you prefer. If that makes sense (to call that “break off” point in the L “the end of the recession” to any economist, I suggest that economist needs to get their examined.

* Last portion of the last sentence in my nearest above comment should read “their head examined.”

I agree with Moses here. Perhaps it would be more appropriate to have two measures: recession and full recovery of median real household income to pre-recession levels.

Of course some would prefer to use stock market recovery or bank profit recovery which were much, much faster than income recovery.

Using real median income household income as a measure might have dissuaded some very serious economists posing as public intellectuals from touting the great Obama recovery prematurely.

Well, it would certainly be pretty surprising if they were to declare that the trough had occurred during any other month, that is for sure.

Now if only they would make an official judgment on what letter the shape of the path of GDP most resembled through all this, that would really answer the most important question that has been so ferociously debated here, :-).

Short but very deep. Let’s hear from the MAGA hat wearers. Shortest recession ever. Most impeachments ever. Trump is their superhero!!!

https://www.cgdev.org/publication/three-new-estimates-indias-all-cause-excess-mortality-during-covid-19-pandemic

July 20, 2021

Excess Mortality during the COVID-19 Pandemic

By Abhishek Anand, Justin Sandefur and Arvind Subramanian

Abstract

India lacks an authoritative estimate of the death toll from the COVID-19 pandemic. We report excess mortality estimates from three different data sources from the pandemic’s start through June 2021. First, extrapolation of state-level civil registration from seven states suggests 3.4 million excess deaths. Second, applying international estimates of age-specific infection fatality rates (IFR) to Indian seroprevalence data implies a higher toll of around 4 million. Third, our analysis of the Consumer Pyramid Household Survey, a longitudinal panel of over 800,000 individuals across all states, yields an estimate of 4.9 million excess deaths. Each of these estimates has shortcomings and they also diverge in the pattern of deaths between the two waves of the pandemic. Estimating COVID-deaths with statistical confidence may prove elusive. But all estimates suggest that the death toll from the pandemic is likely to be an order of magnitude greater than the official count of 400,000; they also suggest that the first wave was more lethal than is believed. Understanding and engaging with the data-based estimates is necessary because in this horrific tragedy the counting—and the attendant accountability—will count for now but also the future.

http://www.xinhuanet.com/english/2021-07/20/c_1310072400.htm

July 20, 2021

Over 1.46 bln doses of COVID-19 vaccines administered in China

BEIJING — More than 1.46 billion doses of COVID-19 vaccines have been administered in China as of Monday, the National Health Commission announced Tuesday.

[ Chinese coronavirus vaccine yearly production capacity is now 5 billion doses. Along with more than 1.46 billion doses of Chinese vaccines administered domestically, another 570 million doses have been distributed internationally. A number of countries are now producing Chinese vaccines from delivered raw materials. ]

I am bemused by the notion that an economic slump (or the opposite) is simply defined as the period from peak to trough.

It really doesn’t seem to have much utility, save as a paper-waving point…

SecondLook: Well, maybe “output gap” is the concept you’re looking for.

Size of the gap matters. Duration also matters. I always like Krugman’s PLOG aka prolonged large output gap in reference to the Great Recession. The gap in 2020 was certainly large but hopefully does not last long.

I don’t believe that would work for me. The output gap – besides being a relatively obscure term outside the professional and well-educated communities – is more theoretical/debatable based on its parameters than Recession which is definitely a popular kind of person on the street term.

As an analogy: the pandemic “officially” ended in January 2021 since that was when reported cases peaked.

He who lives by vector analysis dies by it.

And as Paul Grice said, words do implicate…

How about the idea that a recession is finally over simply when the economy is back to, not any potential peak, but rather to its pre-slump multi-year trend?

I know, not going to be considered as a viable narrative.

SecondLook: Well, there’s such a thing as an “unemployment gap” which you are free to define in any number of ways (and I’m pretty sure most people know what unemployment is).

By the way, Delong and Summers did try something like Friedman’s plucking model, as discussed on this blog a number of times, specifically: [1], [2], [3], [4], [5] [partial listing]. Now using pre-recession multi-year trends might be useful, but as Blanchard and Summers points out, there’ll be a lot of cases where output *never* reverts to pre-recession trend.

@ Menzie

Let me ask you this “joe six pack style question”. What if you had a certain ratio of “reverting” back to GDP trend, let’s say if you had a “end of recession” watermark of 3/4ths back to trend or 7/8ths. If we applied that to the current recession would you be willing to admit that “end of recession” benchmark would create a demarcation of the “end of recession” MUCH closer to describing reality on the ground?????

I mean, Menzie, tell me, with your hand on your heart, if you looked at people’s lives would the 3/4ths return to previous GDP trend as the “end of recession” vs, “the trough” not better reflect people’s real lives and difficulties?? Would you meet me halfway there??~~with all your love of DSGE models or whatever, that that simplicity might better reflect reality??

Moses Herzog: Look, “recession” is a technical term, originated by Burns and Mitchell of the NBER. I could call a “point of inflexion” where “the midpoint of curve” as opposed to “where the second derivative of the function changes”, but that wouldn’t make it right.

@ Menzie

Respectfully~~~ I think I 85% get your argument, even in a roughshod way, I get the math terms. And I can’t say what you are saying is wrong, because it’s not. But on some levels this is what the NBER are saying:

“For many years 10 people shared 10 oranges per day, then one day the fruits got a destructive bacterial disease, and all 10 people had to share one orange per day, over a half year. Then one day things ‘got better’ and the 10 people shared two oranges per day. The recession and bad days were finally over”.

OK. when people read “recession ended after two months” you know what they are thinking?? I can definitively and certainly tell you they are NOT thinking “the second derivative of the function has changed”.

You know what they are thinking, EVEN STILL AFTER THOSE SIX MONTHS (OR TWO MONTHS) HAS ARRIVED???? Menzie, they are thinking “Where the F**K did my whole orange go I used to get every day!?!?!?!? And why is the NBER telling me different???”

That’s what they are thinking Menzie—and it doesn’t put professional economists in a friendly (or even accurate) light in their minds.

Moses Herzog: Yes, this has been a longstanding issue, true when I was an undergrad econ major, and true likely even before that.

You want to characterize a bad time? Then call it a “bad time”, which encompasses how people feel their conditions are. It doesn’t benefit anybody to screw up a definition in order to make people happy.

@ Menzie OK, I’ll call a “truce” on this issue. You’re kind and tolerant to humor my arguments (no sarcasm), and a kind man in general. I appreciate your replies to me (more than I think you perceive). In fact this isn’t a quarrel with you (I guess you don’t see it as a quarrel either) But more a plea for economists to always remember how their words are received by the broader public (which I know many of them do already, just saying.)

“recession is finally over simply when the economy is back to, not any potential peak, but rather to its pre-slump multi-year trend?”

I have seen both of your suggestions being done.

The problem is that both the media and the public use “recession” to mean “the period when the economic activity was low” (for ideosyncratic values of low) instead of “the period when economic activity fell,” thereby ignoring the actual definition. After all, “depression” refers to economic activity being very low, not just dropping, so they think “recession” should be defined in an analogous way.

Personally, I have no problem keeping the noun “recession” as it’s currently defined because it stems from the verb “recede,” and after hitting the trough, economic activity is no longer receding. After all, it’s almost never economists misdefining and misusing “recession.”

I think we need a new word for popular use, a word that kinda means “the period when we think things are crappy” or “the period when everybody has a sad.” That way, the media and the public can define and use the new word any old way they want and leave “recession” for the professionals.

The media has a lot of idiots. Like Ali Velshi knows nothing but that does not stop him from bloviating as if he does.

https://abcnews.go.com/Health/wireStory/fauci-paul-clash-virus-origins-trade-charges-lying-78948911

The battle of wits between Dr. Anthony Fauci and Senator Rand Paul over who is responsible for the origins of COVID-19 had to be fun to watch live. Well – let’s concede it is an unfair match as the junior Senator from Kentucky is one witless clown. Charges of lying we flying as Fauci got to fire off the obvious – Rand Paul does not know what he is talking about. That holds for each and every subject this witless clown goes off on.

“battle of wits between Dr. Anthony Fauci and Senator Rand Paul”

If the Senator is going to insist on a duel with firearms, he really should bring a weapon more powerful than a water pistol.

https://fred.stlouisfed.org/graph/?g=DBg5

January 30, 2018

Real Gross Domestic Product and Real Potential Gross Domestic Product, 2007-2021

(Indexed to 2007)

https://fred.stlouisfed.org/graph/?g=DASi

January 30, 2018

Real Gross Domestic Product and Real Potential Gross Domestic Product, 2017-2021

(Indexed to 2017)

https://fred.stlouisfed.org/graph/?g=DAU4

January 30, 2020

Real Gross Domestic Product and Real Potential Gross Domestic Product, 2020-2021

(Indexed to 2020)

http://krugman.blogs.nytimes.com/2011/01/19/the-output-gap/

January 19, 2011

The Output Gap

By Paul Krugman

Menzie Chinn has a useful post * reminding us just how much output we could and should have been producing is being lost to the slump. He includes this picture:

[Potential and actual GDP, 2007-2011]

What I would add is that these numbers aren’t very different from what we were expecting — or at least what I was expecting — in early 2009. And that’s why I warned from the beginning that the Obama stimulus was too small: **

“For while Mr. Obama got more or less what he asked for, he almost certainly didn’t ask for enough. We’re probably facing the worst slump since the Great Depression. The Congressional Budget Office, not usually given to hyperbole, predicts that over the next three years there will be a $2.9 trillion gap between what the economy could produce and what it will actually produce. And $800 billion, while it sounds like a lot of money, isn’t nearly enough to bridge that chasm.”

Maybe it was politically impossible to do more; we’ll never know. But the same economic logic that said we needed a stimulus also said, right from the beginning, that what we got was deeply inadequate.

* https://econbrowser.com/archives/2011/01/cumulative_outp

** http://www.nytimes.com/2009/02/13/opinion/13krugman.html

It really is a problem that economists need to confront if they want to communicate with the public. If the public doesn’t understand economists use of obscure terms, that’s economists’ fault, not the public’s. And adding another obscure term, output gap, doesn’t help.

There’s a need to distinguish between the economists’ concern about rates and the public’s concern about levels. Some have proposed recession for the former and depression or depressed economy for the latter. Economists should never be allowed to say “the recession is over” without simultaneously saying in the same breath “the depression continues.”

When economists say “the recession is over” and the public says “ivory tower economists are out to lunch, we’re still drowning out here”, that’s a problem economists have to face without just muttering “stupid public.” Economists have an obligation to communicate clearly. And “output gap” or “employment gap” doesn’t do it.

“I think we need a new word for popular use, a word that kinda means “the period when we think things are crappy” or “the period when everybody has a sad.” That way, the media and the public can define and use the new word any old way they want and leave “recession” for the professionals.”

Well, you could use the Great Depression as an example. Pretty much everyone agrees that the Great Depression lasted from 1929 through 1939. Yet according to the NBER, recessions were 1929 to 1933 and 1937 to 1938. There was no recession from 1934 to 1937, yet everyone still calls that part of the depression.

Of course real GDP growth during 1934 to 1936 averaged 11% per year. The problem was that this strong growth was still not enough to counter the enormous decline in real GDP during the Hoover years. So yea we had strong growth during FDR’s first term but were still far from potential GDP when FDR made the mistake of trying to balance the budget in 1937.