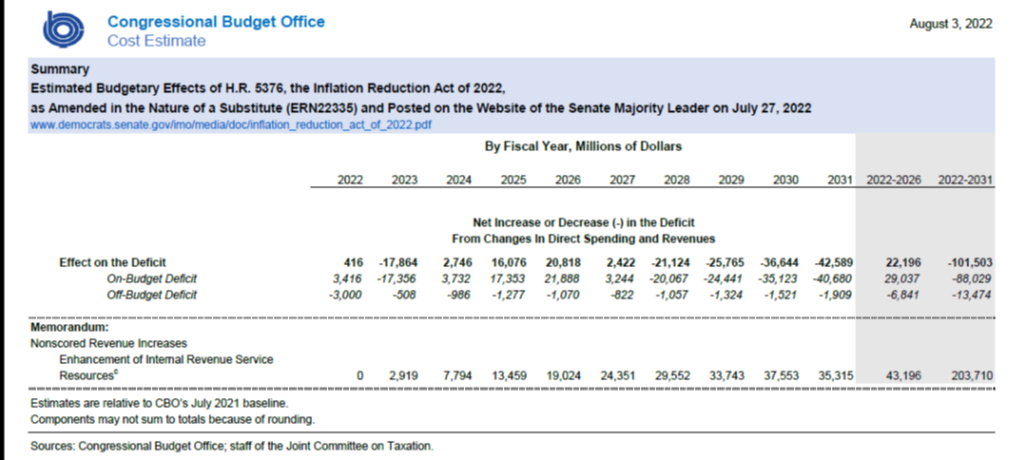

Figure 1: Gasoline price through week ending August 1 (blue, left log scale), price of oil, Brent, through August 1 (red, right log scale). Source: EIA via FRED.

That’s a 15.5% decline since the week ending June 20.

Figure 1: Gasoline price through week ending August 1 (blue, left log scale), price of oil, Brent, through August 1 (red, right log scale). Source: EIA via FRED.

That’s a 15.5% decline since the week ending June 20.

From Goldman Sachs (A.Nathan, J.Grimberg) today:

Despite last week’s Q2 GDP release that showed growth contracting for a second consecutive quarter—tripping the rule of thumb that two quarters of negative growth constitute a recession—we don’t think the US is officially in recession. We note that the indicators that the NBER places the greatest weight on for determining monthly and quarterly business cycle peaks have all continued to increase, as gross domestic income rose in the first quarter and nonfarm payrolls have continued to grow at a rapid pace. And while labor market data has historically lagged other economic indicators, we find that it would be historically unusual for the labor market to appear as strong as it is at present even at the very outset of a recession. We see Q2 corporate financial results and management guidance as providing further evidence that the economic expansion continued during the second quarter, and also view the message from credit market fundamentals as reassuring. That said, growth has slowed substantially, and as a result we continue to expect the Fed to slow the pace of tightening from here, delivering a 50bp hike in September and 25bp hikes in November and December.

Today, we are pleased to present a guest contribution written by Filippo Natoli and Fabrizio Venditti of the Directorate General for Economics, Statistics and Research of the Bank of Italy. The views presented in this note represent those of the author and not necessarily reflect those of the Bank of Italy.

Big daily movement in 10yr, 5yr yields:

UNCTAD’s World Investment Report 2022 came out recently. Figure 1 depicts the recovery of FDI inflows.

With July in, it’s interesting to note that elevated probabilities of recession in 12 months come not from spreads, nor financial conditions, but oil prices.

If one took GDP as the determinant of NBER determined business cycles, this is what the picture would look like (normalizing on mid-Q4):

From Atlanta Fed and IHS Markit:

Is at record highs (at least back to 1947, using latest available data).