The slowdown could be coming from tariffs, or from decelerating economic growth. You decide…

In Bizarro World

Bryan Riley at NTU brings my attention to this press release:

The Coalition for a Prosperous America (CPA) has won the prestigious Edmund A. Mennis Award from the National Association for Business Economics (NABE) for a study showing that a permanent tariff on China would benefit the US economy. The award from the nation’s leading association of business economists confirms a growing acceptance of pro-US trade policies needed to address the nation’s economic challenges.

“Probability of the U.S. or World Entering a Recession in 2020”

I wanted to go to this Society of Government Economists (SGE) event, with Prof. Tara Sinclair (GWU) and Chad Stone (CPBB), but I’m in the Midwest… Fortunately, they shared their thoughts with me.

Nominal GDP Revisions (vs. Others)

Nominal GDP targeting has been proposed as an alternative to the Taylor principle. One challenge to implementation is the relatively large revisions in the growth rate of this variable (and don’t get me started on the level).

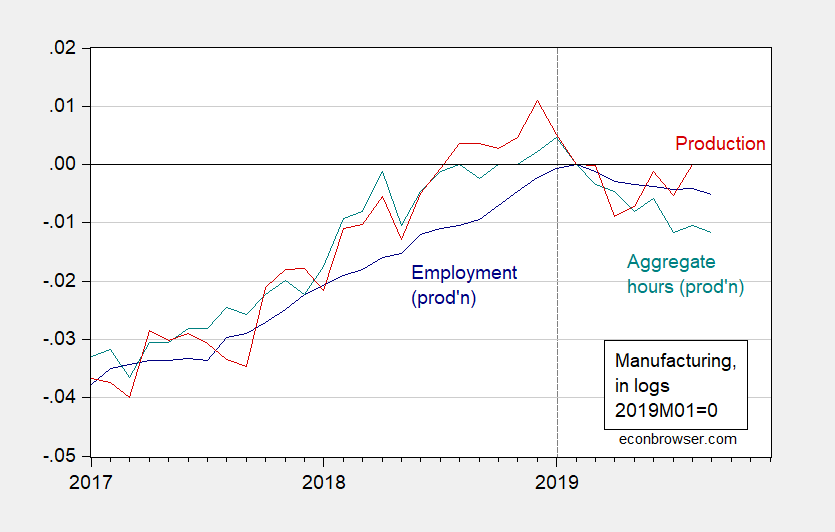

Manufacturing Employment, Hours Decline in September

Figure 1: Manufacturing employment – production and nonsupervisory workers (blue), aggregate hours (teal), manufacturing production (red), in logs 2019M01=0. Source: BLS, Federal Reserve Board, via FRED, and author’s calculations.

Guest Contribution: “It’s Finally Time for German Fiscal Expansion”

Today, we present a guest post written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. A shorter version appeared in Project Syndicate.

Cooperation with “Red China”

Reader Ed Hanson remarks:

Red China has been protectionist since its beginning. [A]nd certainly has since it joined the worldwide trade in the 80’s or so. Did protectionism make it weaker?

In light of Mr. Trump’s remarks today:

“China should start an investigation into the Bidens, because what happened in China is just about as bad as what happened with Ukraine.”

What do people like Ed Hanson (I’m guessing old, and still worrying about Commies, but thinking Russians are ok) think Mr. Trump should bargain away in terms of trade sanctions on “Red China” in order to get that investigation?

James Hamilton at UW Madison: Predicting the Next Recession

The video of Jim Hamilton’s inaugural Juli Plant Grainger Institute lecture at the University of Wisconsin-Madison Economics is now up!

Click here for YouTube video.

Must see for anybody who is serious about critically reading the tea leaves regarding an incipient recession (Spoiler: As of 9/11, he was sceptical a recession had begun). Interesting conjecture about using holding period returns on Treasury securities of different maturities to isolate a expectations hypothesis of term structure component (my reading).

(Aside: for conventional wisdom, see my Econ 435 notes for Econ on EHTS/yield curve/recession prediction)

John Williams on monetary policy and the current economic outlook

I moderated a discussion this morning with John Williams, president of the Federal Reserve Bank of New York, in which John shared his perspectives on monetary policy and the current economic outlook. You can watch on Youtube (conversation begins at 44 minutes in).

Soybeans: Victory Is Around the Corner

On July 9, 2018, about 14 months ago, reader CoRev wrote:

Those of us arguing against the constant anti-tariff, anti-Trump dialogs have noted this will probably be a price blip lasting until US/Chinese negotiations end. We are on record saying the prices will be back approaching last year’s harvest season prices.

Hah, hah, hah, hah! Time to look at prices relative to March 23, 2018, when Trump announced imposing Section 301 tariffs on Chinese goods…