An argument increasingly being made is that inflation is being built into wage demands in a context of really tight labor markets, and this would induce a wage-price spiral. This outcome is plausible, but I think it’s useful to compare wages against CPI to see if wages are really abnormally high, and are starting to rise in tandem with inflation. [text corrected 8/13]

Business Cycle Indicators and Retail Sales as of Mid-July 2021

Industrial production was released yesterday, and retail sales today.

Wisconsin Manufacturing Employment and Manufactured Exports

Does Wisconsin’s fortunes — as a manufacturing heavy state — depend on what happens in the rest-of-the world? The answer is, partly, yes…

Inflation Expectations of Consumers

A lot of coverage of how the NY Fed’s survey of consumers’ inflation expectations had moved substantially (e.g. NYT). A couple of observations: (1) household/consumer based expectations are upwardly biased; (2) the high inflation is expected to be temporary, in the sense that the expected inflation in the next 12 months is higher than 12 month inflation ending in June 2024.

Wisconsin Employment in June 2021: Halting Growth Continues

Employment numbers for June were released for today.

“Do Central Banks Rebalance Their Currency Shares?”

Paper by me, Hiro Ito, and Robert McCauley. From the abstract.

“The impact of lockdowns on international trade”

PPI and CPI for June

From Reuters today:

Public Service Announcement: Real Rates Are (Still) Low

If demand is so high, why are real rates so low (even admitting Fed QE, forward guidance, etc.)?

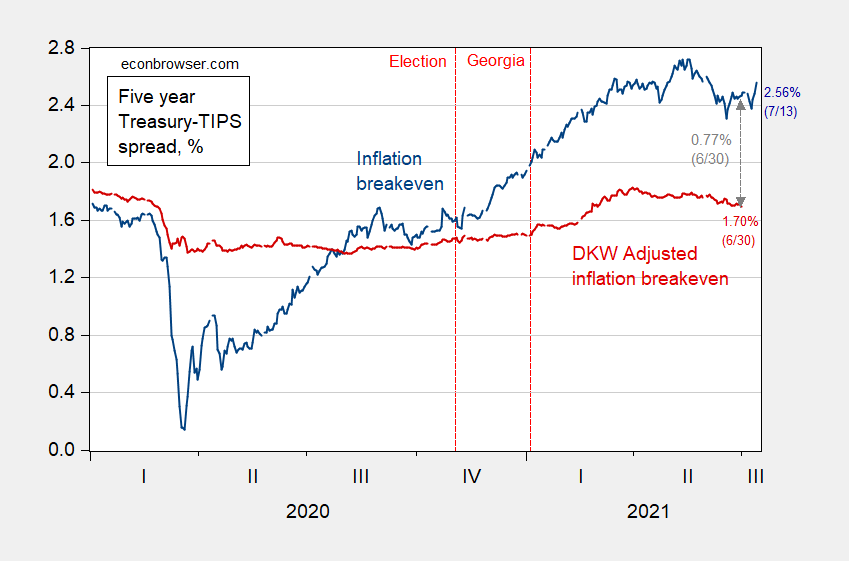

Inflation Breakevens for 5 Year Horizon

As of 7/13:

Figure 1: Five year inflation breakeven calculated as five year Treasury yield minus five year TIPS yield (blue, left scale), five year breakeven adjusted by inflation risk premium and liquidity premium per DKW (red, left scale), both in %; and S&P 500 index (black, right log scale). Source: FRB via FRED, Treasury, KWW following D’amico, Kim and Wei (DKW) accessed 6/4, and author’s calculations.

The 5 year breakeven increased by 8 bps going from yesterday to today (I’m taking the “news” as the CPI surprise discussed here); and remains 16 bps below the recent peak on 5/18. That 8 bps increase is pretty substantial since the standard deviation of daily changes is about 4 bps since 2000 (excluding the extreme movements in 2008).