Here’s a time series of the real minimum wage, under the Sanders proposal.

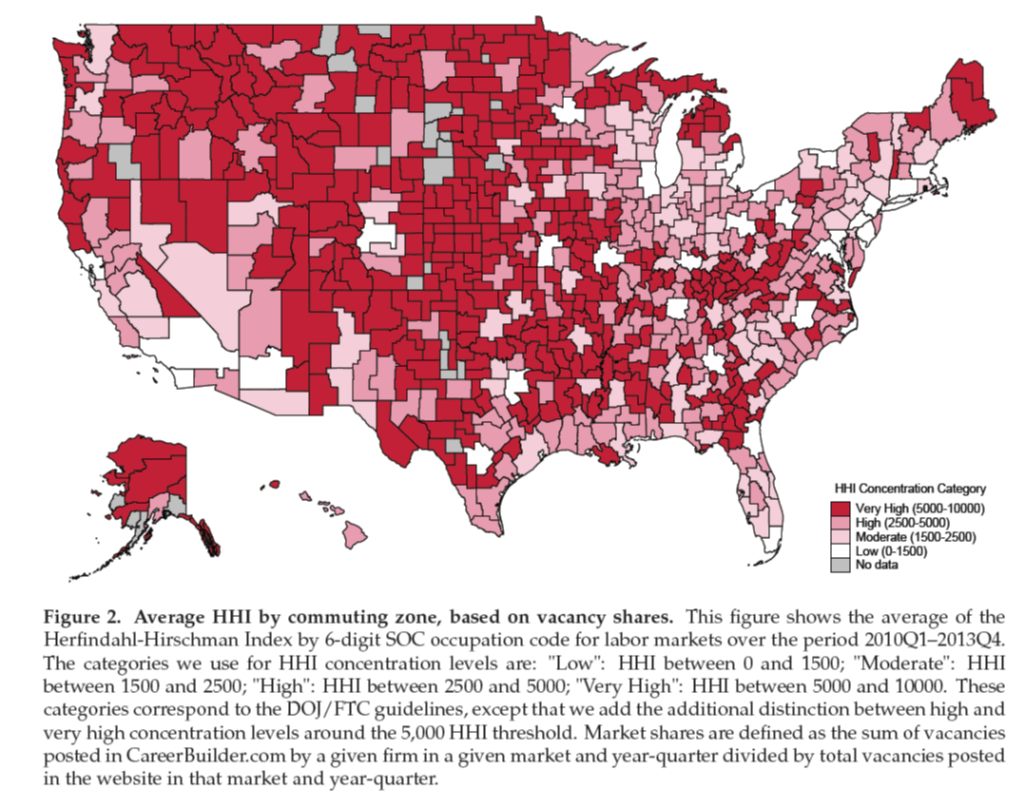

Labor Market Monopsony Estimated

Azar, Marinescu, Steinbaum (2018) as SSRN [NBER WP version] [preprint at J.Human Resource]:

Addendum, 2/8 8am Pacific:

And here is a very recent survey of labor market monopsony: Manning, ILR (2021).

Guest Contribution: “What the GameStop Bubble Says about Financial Markets”

Today, we present a guest post written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. A shorter version appeared at Project Syndicate.

The University of California gives back to the community

About 10% of the population in San Diego have now received the vaccine. A third of these — 100,000 people– were served by a single facility operated by the University of California at San Diego. What’s the secret to their success? Answer: logistics.

Continue reading

The Employment Deceleration, and Business Cycle Indicators

Employment in early January continues to decelerate to near standstill (BLS), as I suggested in November would happen if the US did not implement a coherent plan to contain the Covid-19 pandemic.

A Review of Minimum Wage Effects

From Alan Manning, in Journal of Economic Perspectives (a journal of the American Economic Association), “The Elusive Employment Effect of the Minimum Wage”:

The American Rescue Plan Assessed

I talked through some issues regarding the competing recovery plans in this Wisconsin Public Radio interview. Here are some graphs to buttress my point that the Senate Republican plan is underpowered.

CBO’s Outlook and the Output Gap

CBO released its projections for GDP under current law, and potential GDP yesterday.

Flash-mob finance

Modern communication infrastructure can facilitate swift simultaneous action by a large number of people. If used to coordinate a surprise attack, an organized mob can overcome a store or even the capitol building. Is Wall Street the next target?

Continue reading

The Economy at Trump’s End

In recovery (as Jim noted using GDP), but not recovered. And maybe even declining for certain key indicators.