Republicans and lean Republican respondents really, really, really don’t like economic conditions right now, switching “bigly” upon Trump’s election, contributing an outsize impact on the overall University of Michigan consumer sentiment index. Democrats and lean Democratic respondents think things are about the same as mid-2016 (under Obama).

Are You Better Off than You Were Four Years Ago?

GDP per capita, consumption per capita, disposable income per capita, unemployment, economic policy uncertainty, VIX, and Misery Index — plus median household income.

Confidence, Sentiment, and News in April: Some Time Series

Sharp reactions to Conference Board consumer confidence index today. Here’s some context for this movement, as well as that in the U.Michigan survey of economic sentiment.

Four Measures of the Output Gap and Measuring Trends

Talking about a rethink of the output gap, and the concept of the trend-cycle decomposition in macro policy tomorrow. Here’s a picture of the output gap from CBO, from two statistical filters (Hodrick-Prescott and Fleischman-Roberts/Fed Board), and the Delong and Summers (BPEA 1988) model.

California in Recession (?)

That’s the almost gleeful conclusion in an article in the Washington Examiner last December. Now, it’s true they based that conclusion on a Legislative Analyst’s Office report. However, that conclusion was based on the (inappropriate) use of the (national level) Sahm rule to state level unemployment rates. And as Dr. Sahm has remarked, this is not the right way to go — rather one needs to examine the appropriate threshold for a given state before using it to infer a recession.

Wouldn’t It Be Nice…

That’s the song I was thinking about when I saw the headline in the WSJ, Trump Allies Draw Up Plans to Blunt Fed Independence:

US Oil Production in 2023, Net Exports of Petroleum Products through 2024Q1

From EIA, and BEA NIPA:

Stagflation Fears? March NBER Business Cycle Indicators and Instantaneous Inflation

That’s a term that is invoked in a CNN article today. I think of stagflation as weak growth combined with high inflation. A little context:

GDP, Nowcasts, and Est’d GDO, GDP+, and Final Sales

Following up on Jim’s post yesterday, thoughts on measurement error and prospects. Note that GDP surprised on the downside, at 1.6 ppts q/q AR vs. consensus 2.5 ppts. On the other hand, GDP+ grows faster, as does final sales to private domestic purchasers.

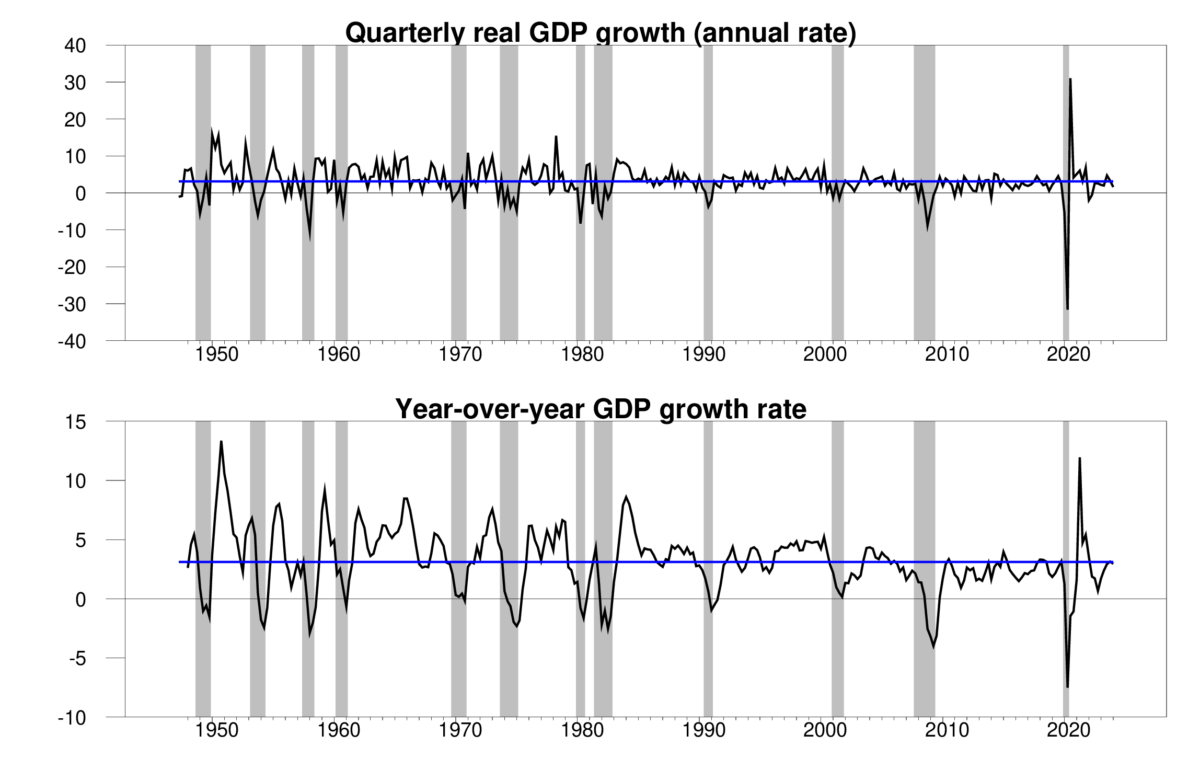

Almost landed

The Bureau of Economic Analysis announced today that seasonally adjusted U.S. real GDP grew at a 1.6% annual rate in the first quarter. That’s a little lower than many analysts expected. But the year-over-year growth is still on track.

Top panel: quarterly real GDP growth at an annual rate, 1947:Q2-2024:Q1, with the historical average (3.1%) in blue. Calculated as 400 times the difference in the natural log of real GDP from the previous quarter. Bottom panel: year-over-year growth rate. Calculated as 100 times the difference in the natural log of real GDP from the same quarter of the previous year.