Comparing CDC tabulated Covid-19 fatalities, excess fatalities, and unofficial data (an update to this post).

Is Florida In for a W?

I see Governor DeSantis say all is under control, as the Florida economy remains largely open. Economic activity as of mid-June did recover. But Covid-19 surges suggest a retrenchment in the future; the extent of this will depend on how much the epidemic progresses, and what the governor’s tolerance for fatalities/day is.

Nowcasting Q3

Believe it or not, we’re in the 3rd quarter. IHS/Markit (née Macroeconomic Advisers) informs me:

Inferring Covid-19 Fatalities

If you look at the CDC statistics without looking at the footnotes, you could be forgiven for mistakenly concluding the US was nearing zero Covid-19 fatalities.

Wisconsin Employment in June…and the Course of Covid-19

Nonfarm payroll employment slightly exceed June 22 Economic Outlook forecast.

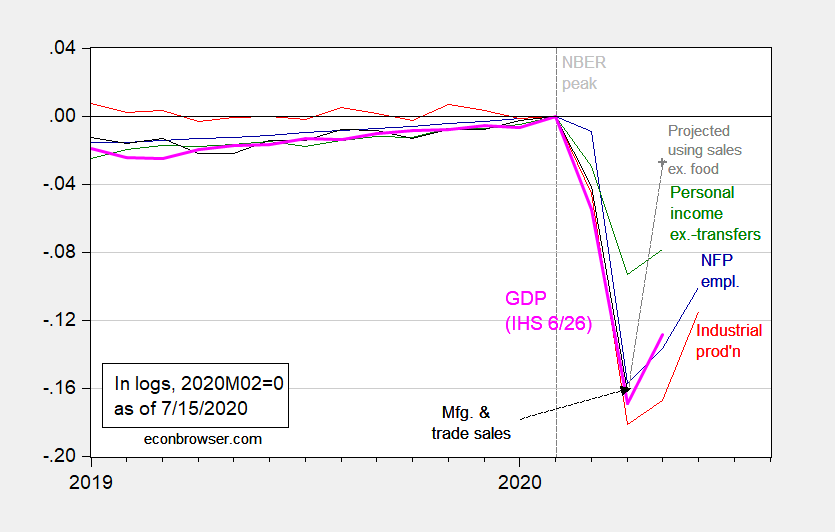

Business Cycle Indicators as of 15 July 2020

Industrial production numbers are out today. Here are five key indicators referenced by the NBER’s Business Cycle Dating Committee.

Figure 1: Nonfarm payroll employment (blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), and monthly GDP in Ch.2012$ (pink), all log normalized to 2019M02=0. May observation for manufacturing and trade sales projected using log-linear regression of sales on retail sales ex.-food services over the 2019-20M04 period. Source: BLS, Federal Reserve, BEA, via FRED, Macroeconomic Advisers (6/26 release), NBER, and author’s calculations.

If one were convinced that these indicators (along with many others) were going to continue to trend upwards, one could imagine a recession declared as starting in 2020M02 (NBER peak) and ending in 2020M04 (trough). However, if there were to be a relapse in some of the indicators in July-August (see discussion here), one could imagine a longer contraction eventually being declared (some accounts say there’s an increasing view in the Fed along these lines).

Recessions vs. Negative Output Gaps

Two observations: (i) recessions do not necessarily coincide with negative output gaps (although they do seem to coincide with the beginning of periods of negative output gaps); and (ii) recoveries do not always coincide with positive output gaps. [This is an update of a 2008 post.]

Chinn-Ito Index, Updated to 2018

Open Letter to Lawmakers: “On Recovery Policy”

From Scholars Strategy Network, an open letter:

Economists’ Letter on Recovery Policy

Dear National Lawmakers,As you consider a new package of aid to support the nation during the ongoing COVID-19 pandemic, now is an appropriate time for the federal government to consider economic research carefully in order to provide well-targeted, significant relief to state governments and to individuals experiencing economic hardship. Support for state budgets, and for safety net programs, most notably funding for the Supplemental Nutrition Assistance Program (SNAP) and for Unemployment Insurance, are wise ways to do this.

An Improved GDP Outlook from Wall Street

The Wall Street Journal’s July survey results are out. The forecasted level of GDP is higher despite the deteriorating Covid-19 infection and fatality numbers.